From the Research Lab: Why Lower Interest Rates Might Cool Inflation Instead of Fueling It

WHY LOWER INTEREST RATES MIGHT COOL INFLATION INSTEAD OF FUELING IT

As the Fed considers a September rate cut, new Columbia Business School research shows that lower interest rates may reduce rents, cooling one of the biggest drivers of U.S. inflation.

by Boaz Abramson, Assistant Professor of Business, Finance Division

September 2025

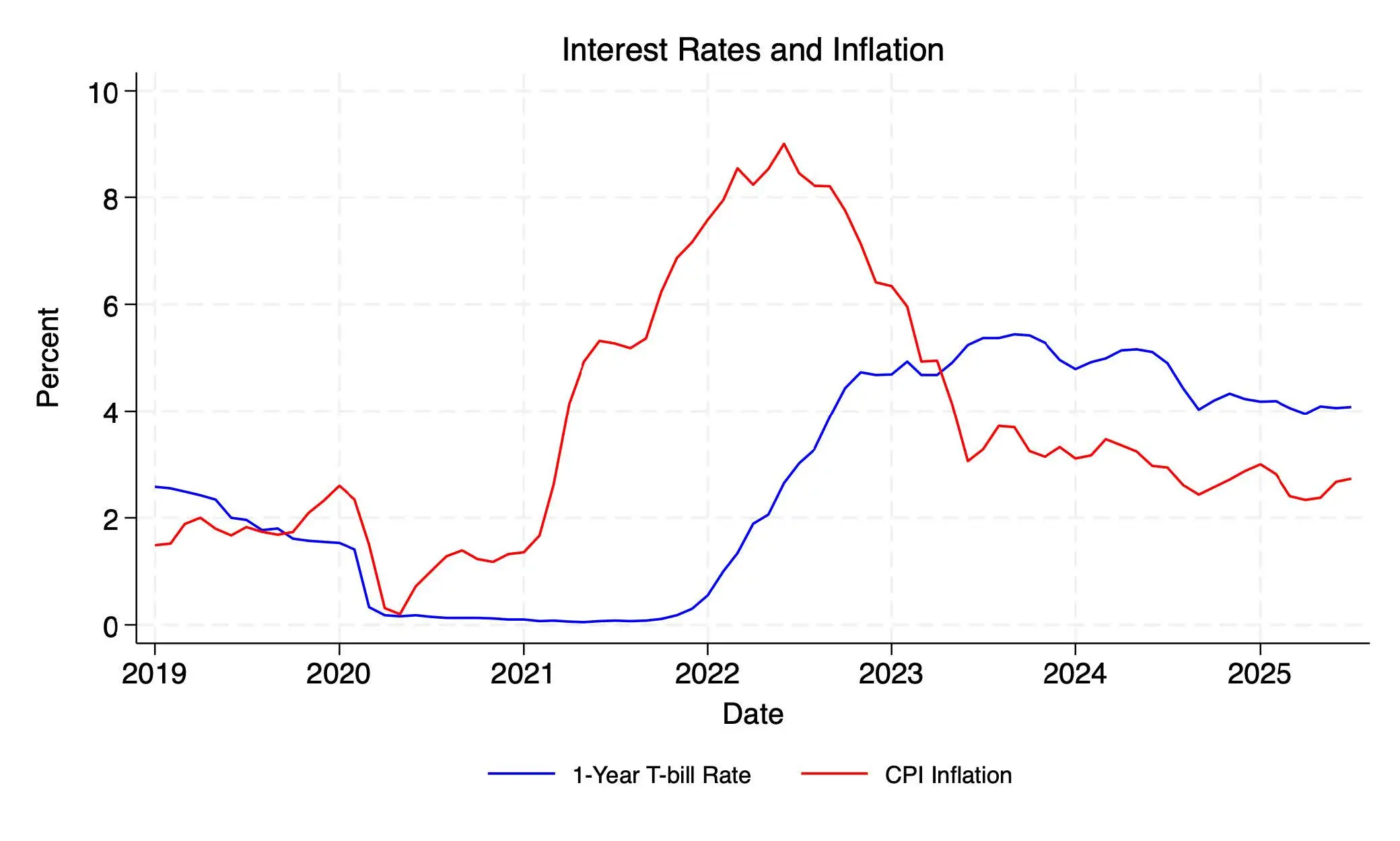

All eyes are on the September Federal Open Market Committee meeting. At his Jackson Hole, Wyoming, speech, Federal Reserve Chair Jerome Powell opened the door to a potential rate cut, indicating that deteriorating labor market conditions might warrant a change in the Fed’s policy stance. Markets reacted strongly to the dovish comments: the Dow, S&P 500, and Nasdaq all surged, while Treasury yields plummeted. However, many economists, including Fed officials, are wary of cutting rates at a time when inflation is still well above its 2 percent target. Indeed, despite high interest rates, inflation remains stubbornly above what the Fed would like it to be. Powell himself stressed the need to "proceed carefully" given the continued inflationary risks.

A key component of overall inflation is rent. The consumer price index (CPI), which is compiled by the Bureau of Labor Statistics (BLS) and tracks price movements of a representative basket of goods and services, is composed of eight major components. The shelter component, which measures the cost of housing, is the largest component and accounts for roughly 35 percent of the CPI. The CPI shelter index reflects the price of housing for both renters and homeowners but, importantly, is based entirely on rental data. The cost of housing for owner-occupiers is measured as the rent that homeowners would have paid had they rented their home and is imputed from BLS rental data as an “owner-equivalent rent.” This means that more than one-third of overall inflation in the U.S. is due to rent inflation. The extent to which interest rate cuts translate into higher inflation therefore crucially depends on how interest rates impact rents.

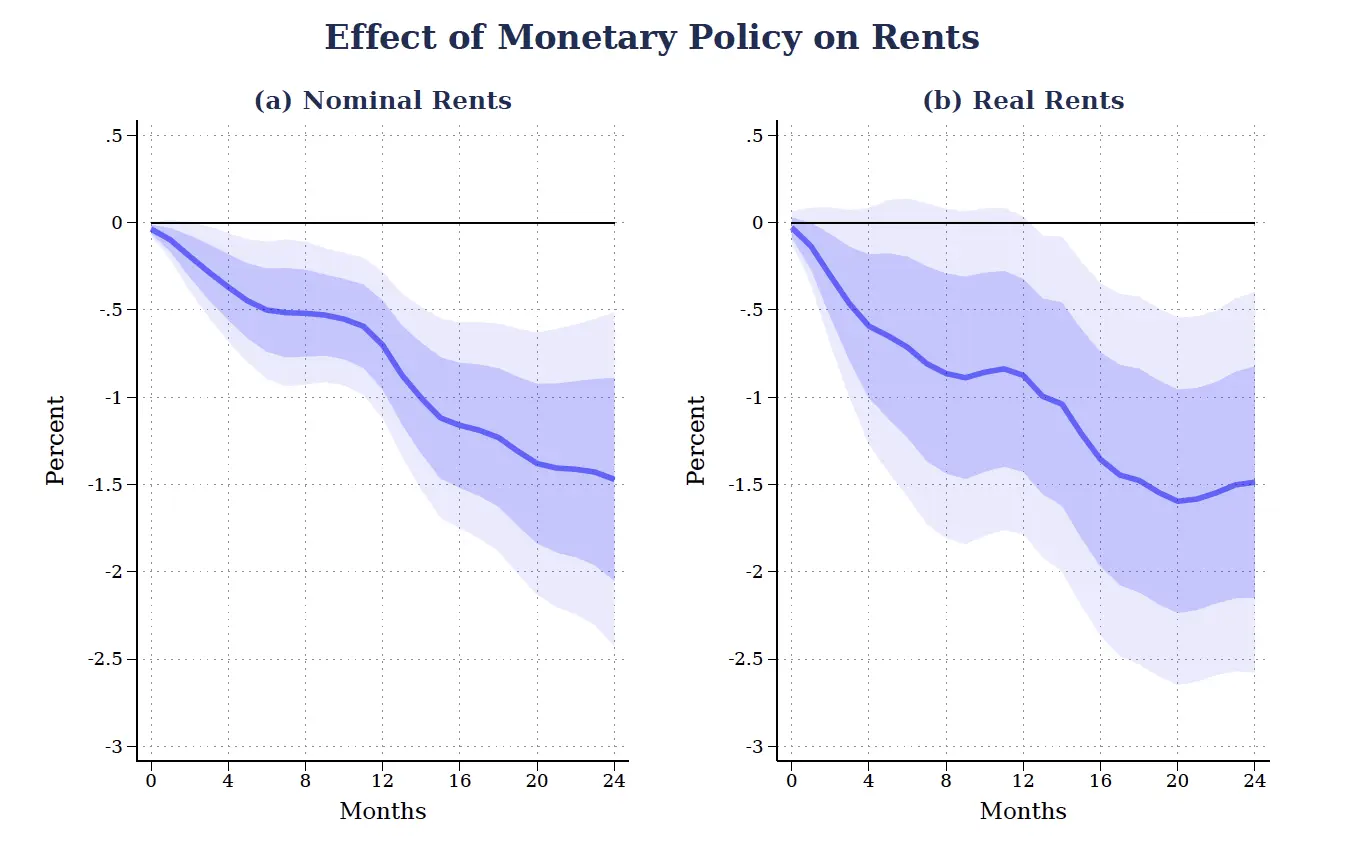

The fear is that by lowering interest rates, the Fed may stimulate the economy and increase inflation. The surprising finding in new research from Columbia Business School is that lower interest rates can lower rents instead of increasing them. The study, which I have coauthored with Pablo De Llanos of Columbia University and Lu Han of University of Wisconsin, finds that a 0.25 percentage point drop in the 30-year fixed mortgage rate leads to a 1.4 percent decrease in nominal rents and a 1.6 percent decrease in real rents. In other words, by lowering rents, expansionary monetary policy can actually cool inflation.

Why do rents drop in response to expansionary monetary policy? When interest rates drop, borrowing becomes less expensive, making it easier for many households — especially first-time and lower-income buyers — to purchase homes. As a result, more people exit the rental market, lowering demand for rental housing and placing downward pressure on rents. Our results show that as demand for owner-occupied housing increases and demand for rental housing drops, real estate investors sell homes to owner-occupier households. The homeownership rate increases, house prices increase, and rents decrease.

To conduct our analysis, we developed a new residential rent index, the ADH Repeat-Rent Index, which measures changes in rent prices over time on a quality-adjusted basis. We compiled a dataset of more than 30 million rental listings, covering over 5,000 ZIP codes across the United States. Using this data, and applying a statistical technique known as local projections, we estimate how rents change in response to monetary policy shocks—unexpected changes in interest rates. Figure 2 illustrates our main results. It plots how a 25-basis-point decrease in the 30-year fixed rate mortgage impacts rent inflation 0-24 months going forward. A drop in mortgage rates lowers nominal rent inflation by 0.7 percent 12 months following the rate cut, and by 1.4 percent 24 months following the cut. In the paper, we also find that following a drop in interest rates, the inventory of rental units increases, and units remain listed on the market for longer. This indicates a drop in demand in the rental market and rationalizes why lower rates lead to lower rents.

With the next FOMC meeting in sight, policymakers will be monitoring how tariff policies are transmitted into prices and whether deteriorating labor market conditions persist. A key indicator that policymakers should also be tracking is rent inflation. In its most recent July reading, annual rent inflation according to the CPI shelter index was 3.7 percent — well above the Fed’s 2 percent target. Overall inflation might increase if the Fed decides to cut rates, but our analysis shows that expansionary policy can cool rent inflation, softening the blow.

References:

Abramson, Boaz, Pablo De Llanos, and Lu Han. 2025. “Monetary Policy and Rents.” Working paper, Columbia Business School and University of Wisconsin-Madison

About the Contributor:

Boaz Abramson is an assistant professor in the finance division at Columbia Business School. He received his Ph.D. in Economics from Stanford University in 2022, and holds a MA and BA from the Hebrew University of Jerusalem.

His research lies in the intersection of macroeconomics, housing, and finance. He is particularly interested in the housing insecurity problem in the US rental market, where millions of renters are evicted every year and where homelessness is pervasive. His recent work examines how instating stronger tenant protections against evictions impacts rents, homelessness, and evictions.Full bio here.