From the Research Lab: The Future of Residential Real Estate Transactions: How Technology & Regulation Are Reshaping the Market

New commission rules, platform consolidation, and generative AI are pushing U.S. housing toward a more digital, consumer-centric future. But structural frictions continue to slow the path to fully automated closings.

by Tomasz Piskorski, Edward S. Gordon Professor of Real Estate, Finance Division

October 2025

For years, the U.S. housing market has seen waves of innovation—from online listings to digital mortgages to instant offers—but the pace of transformation has been slower and more uneven than in sectors like retail, banking, or travel. Despite real demand for convenience and transparency, structural frictions have kept the transaction process largely intact.

Three recent developments suggest that change may be accelerating. First, the National Association of Realtors (NAR) settlement challenges the long-standing commission structure, opening the door to new compensation models. Second, Rocket Companies’ acquisition of Redfin signals a renewed push toward vertically integrated, tech-enabled real estate platforms designed to streamline the entire transaction process. Finally, the rise of generative AI and conversational interfaces adds new momentum to this shift, promising to simplify and automate further tasks like search, customer service, and document preparation. These shifts point toward a more digital, consumer-centric future—but they also sharpen a deeper question: what drives real estate innovation, and why has it often fallen short?

Innovations So Far

Over the last two decades, a series of innovations have aimed to simplify, digitize, or disrupt various parts of the housing transaction. Zillow changed how people search for homes by democratizing listing access and home value estimates. Redfin positioned itself as a tech-enabled brokerage, aiming to make agents more efficient through salaried employment, centralized support, and integrated digital tools, while offering buyers built-in commission rebates. Rocket Mortgage (formerly known as Quicken Loans) made mortgage applications fast and mobile-friendly, becoming the largest mortgage lender in the country. And most recently, iBuyers like Opendoor, Zillow Offers, RedfinNow, and Offerpad attempted to introduce instant home sales using pricing algorithms.

What Drives Real Estate Innovation?

As my work shows, real estate innovation is driven by one clear factor: consumers value convenience and speed and are willing to pay for it. I found that fintech mortgage lenders like Rocket didn’t compete by offering lower interest rates; they actually charged more—on average 14–16 basis points higher than traditional bank lenders—but won market share by offering a faster and easier digital borrowing process. Borrowers valued time, certainty, and simplicity over marginal savings. This same dynamic helps explain the rise of iBuyers, who purchase homes directly through online platforms. My analysis of transaction records shows that many sellers are willing to accept a 3 percent price discount on average in exchange for avoiding the traditional sales process. The speed and certainty of an instant offer carry real economic value.

Key Challenges to Innovation

Each of the innovations so far addressed real pain points—friction, opacity, paperwork, and slowness—but most collided with the same challenge: housing is complex, locally variable, and emotionally charged. Unlike, say, selling books on Amazon or ordering Uber rides, home sales are infrequent, meaning there are few repeat customers to build ongoing relationships or brand loyalty. It is also the single largest financial decision most households make, and one they face only rarely. On top of that, housing markets are highly fragmented across regions, with different legal, regulatory, and institutional structures. And homes themselves are not uniform products: every property is unique, with quirks and features that make valuation difficult—and that different consumers may value in very different ways. Pricing a house isn’t like pricing a car or a phone—two homes on the same street can differ in condition, layout, backyard quality, and so on. This combination of high stakes, low individual transaction frequency, local fragmentation, and the inherently idiosyncratic tastes makes real estate far harder to automate and standardize than almost any other major consumer transaction.

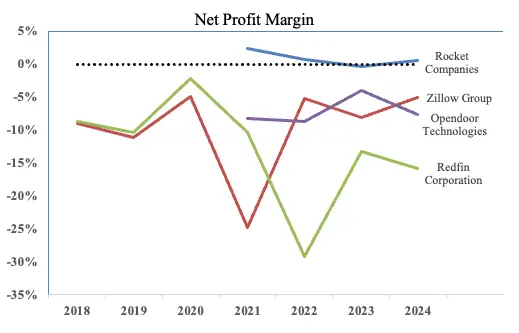

These challenges also help explain why most leading real estate tech companies have struggled with profitability. As the figure shows, Zillow and Opendoor have operated with persistently negative margins, generally in the range of –5 to –15 percent, underscoring how difficult it is to achieve profitability even at scale. Redfin stands out for its volatility, with margins plunging to nearly –30 percent in 2022 before partially recovering, though still remaining negative. Only Rocket Companies has consistently maintained margins above or close to break-even. Taken together, these trends highlight that while these firms have grown in prominence and reshaped aspects of the housing market, most remain unprofitable, reflecting the structural challenges facing technology-driven real estate businesses. On the other hand, these businesses are still in a growth phase, and, as the example of Amazon demonstrates, it can take time before such firms achieve sustained profitability.

Source: Bloomberg, Capital IQ Pro, 10-K reports. The net profit margin is defined as net income divided by revenue.

Source: Bloomberg, Capital IQ Pro, 10-K reports. The net profit margin is defined as net income divided by revenue.

But my research also highlights the additional constraints. Rocket (formerly known as Quicken Loans) became the largest residential lender in the U.S. because it specializes in an activity that faces limited adverse selection: issuing loans guaranteed by government-sponsored enterprises (GSEs). It also does not need much capital as it can quickly sell these loans in the agency MBS market. This explains why Quicken became the largest residential lender despite not having the deposit funding advantage afforded to traditional banks.

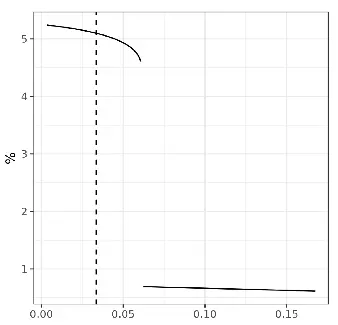

Automating transactions where adverse selection concerns are real is much harder. As my work shows, iBuying works best for homes that are easy to value—newer, standardized properties in liquid markets. Where homes are more idiosyncratic or harder to price, the model breaks down—even if the algorithmic pricing models are fairly accurate. A seemingly small valuation error of just above 5 percent of a home’s value can be enough to attract sellers with problematic or overpriced properties, who are more likely to use an iBuyer. This creates adverse selection, which reduces margins and increases losses leading to a collapse in iBuyer market share (see figure below).

iBuyer Market Share as a function of the algorithm valuation error

Source: Buchak, G., G. Matvos, T. Piskorski, and A. Seru. (Forthcoming). Why is intermediating houses so difficult? Evidence from iBuyers. Journal of Political Economy.

Source: Buchak, G., G. Matvos, T. Piskorski, and A. Seru. (Forthcoming). Why is intermediating houses so difficult? Evidence from iBuyers. Journal of Political Economy.

As my work anticipated, Zillow exited iBuying in 2021 after nearly $900 million in losses, and Redfin followed by shutting down its program in 2022. Despite the appeal of convenience and consumer willingness to pay for it, the combination of algorithmic pricing and an online home-acquisition platform proved difficult to execute.

The NAR Settlement: A Structural Reset?

In addition to technological disruptions, there are important recent regulatory shifts reshaping the real estate agent industry. Recent court decisions, culminating in the March 2024 National Association of Realtors (NAR) settlement, aim to increase transparency and competition by targeting buyer-agent fees. The settlement removes the requirement for listing agents to offer compensation to buyer’s agents through the MLS, mandates written agreements with clear and negotiable compensation terms, and prohibits vague fee language or filtering listings based on commission.

These regulatory shifts are expected to raise consumer awareness of agent costs, intensify competition, and place downward pressure on commissions—particularly on the buyer’s side—though evidence of significant declines remains limited so far. Over the longer term, these changes could drive a broader reduction in agent fees and, when combined with technological innovations, reshape buyer–seller interactions by compressing costs further and fostering the growth of integrated, AI-assisted real estate agent services.

In the residential leasing market, legislation such as the Fairness in Apartment Rental Expenses (FARE) Act—which took effect on June 11, 2025, in New York City, and prohibits landlords and their agents from charging broker fees to tenants—could also accelerate the adoption of streamlined, AI-assisted rental broker services in the leasing market.

What Comes Next? Integration and the Holy Grail of Digital Closing

The Rocket–Redfin deal signals a strategic bet on what many in the industry see as the holy grail of real estate technology: fully digital closing. In this vision, consumers could browse listings, get pre-approved for financing, tour homes, make offers, and close—all through a single platform, without ever touching paper or interacting with multiple service providers.

In theory, this model promises a seamless experience. And vertically integrated platforms like Rocket–Redfin may be well positioned to deliver it given their combined customer base of millions of households. But in practice, digital closing remains elusive.

Closing remains slow because the system is fragmented—and because legal, regulatory, and financial risks are high. Even with e-signatures and remote notarization, delays in appraisals, inspections, and municipal compliance persist. Consumers may want speed—but they also want trust, advice, and assurance. And so, while progress continues toward streamlining large parts of the process, fully automated closings will likely remain elusive in the foreseeable future, limited by both institutional complexities and consumer behaviors.

References:

Buchak, G., G. Matvos, T. Piskorski, and A. Seru. (2018). Fintech, regulatory arbitrage, and the rise of shadow banks. Journal of Financial Economics 130, 453–483.

Buchak, G., G. Matvos, T. Piskorski, and A. Seru. (Forthcoming). Why is intermediating houses so difficult? Evidence from iBuyers. Journal of Political Economy.

CBS News, March 2024, “What to know about changes to real estate agent commissions”

CBS News, June 2025, “NYC ends broker fees for renters, but will that lead to higher rent prices?”

CNN, March 2024, “Could real estate go the way of the travel industry? Not quite”

MarketWatch, August 2024, “Would lower real-estate commissions lead to higher home prices? Economists are split”

MarketWatch, March 2025, “Rocket-Redfin deal could make home buying more convenient — and more expensive”

FAQs:

Q: What are the main forces driving change in residential real estate transactions?

A: New regulatory shifts like the NAR settlement, technology consolidation such as Rocket’s acquisition of Redfin, and the adoption of AI tools are accelerating innovation in the housing market.

Q: Why has real estate innovation often lagged behind other sectors?

A: Housing transactions are complex, infrequent, and highly localized. Each property is unique, legal frameworks vary by state, and the stakes are much higher than in retail or travel. These factors make automation and standardization more difficult.

Q: What is the “holy grail” of real estate technology?

A: A fully digital closing process, where buyers and sellers can complete every step—from listing to financing to final signatures—on a single integrated platform. While progress is being made, institutional complexity and consumer trust needs mean it remains a long-term goal.

About the Contributor:

Tomasz Piskorski is the Edward S. Gordon Professor of Real Estate in the Finance Division at Columbia Business School. He is also a Research Associate at the National Bureau of Economic Research and serves on the Academic Research Council of the Housing Finance Policy Center at the Urban Institute. Professor Piskorski earned a M.S. in Mathematics from New York University Courant Institute of Mathematical Sciences and a Ph.D. in Economics from New York University Stern School of Business.

Professor Piskorski’s research explores issues in real estate finance, securities and mortgage markets, financial intermediation and banking, market structure and regulation, and housing policy. His recent work centers on inefficiencies in credit markets, financial technology, shadow banking, financial regulation, mortgage market reform, and the impact of consumer credit markets on the broader economy. Full bio here.