From the Research Lab: The Affordable Housing Paradox

Why low-rent properties deliver high returns—and why investors stay away.

by Stijn Van Nieuwerburgh, Earle W. Kazis and Benjamin Schore Professor of Real Estate, Finance Division; Co-DIrector, Paul Milstein Center for Real Estate

November 2025

Few issues loom larger in today’s policy debates than the lack of affordable housing. Rent burdens have risen steadily across advanced economies, leaving low-income tenants with little financial breathing room. In the US, 50 percent of renters spend more than 30 percent of their income on housing, and nearly 30 percent are severely rent-burdened, devoting over 50 percent of income to rent. The pressure is highest at the bottom of the market. Similar patterns emerge in the Netherlands and Belgium.

Conventional wisdom says these properties make a poor investment for landlords because they often involve lower-income tenants, aging buildings, and higher maintenance costs. Yet new evidence tells a different story. Our recent study spanning Belgium, the Netherlands, and the US shows that properties in the lowest rent tier consistently earn the highest returns.

This finding seems to run counter to common sense. Rather than being a charity case, affordable housing may actually contain hidden alpha for investors.

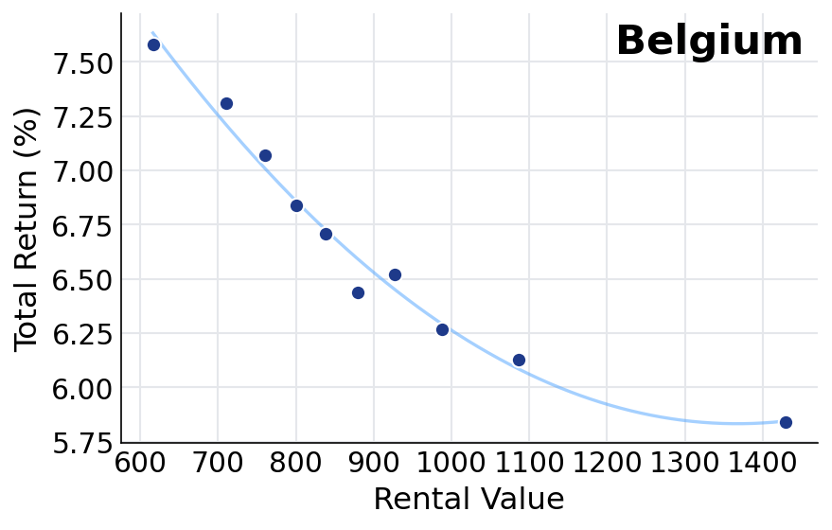

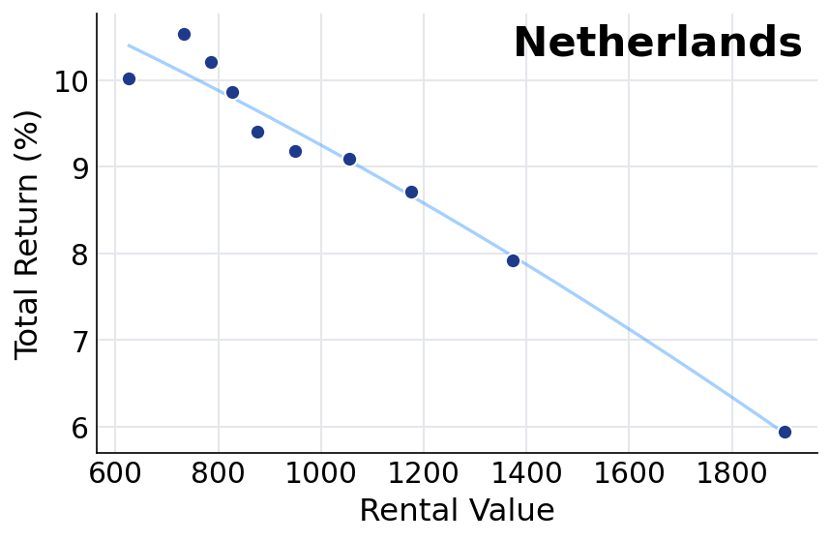

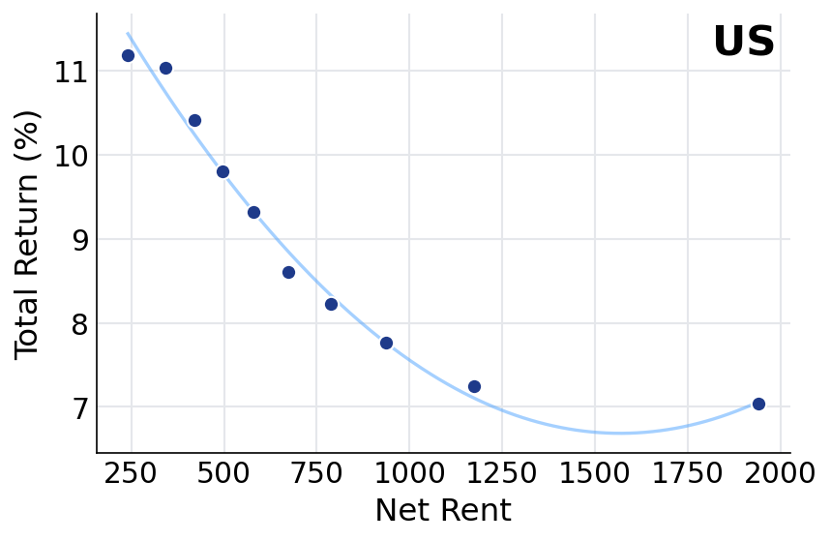

Key Findings: Higher Returns at the Bottom

The data, drawn from millions of leases and sales records, reveal a striking pattern:

- Rental Yields: In the US, the lowest-rent multifamily properties earn net yields about 0.6 percentage points higher per year than the highest-rent units. In Belgium, the spread is 0.9 percent, and in the Netherlands, it is even larger at 1.1 percent.

- Capital Gains: Beyond rental income, low-rent properties appreciate faster. Price growth in the lowest decile beats the top by 3.6 percent in the US, 0.8 percent in Belgium, and 3 percent in the Netherlands.

- Total Return: When combined, the advantage is substantial: +4.2 percent in the US, +1.7 percent in Belgium and +4.1 percent in the Netherlands per year.

The figures below show a clear downward slope: the cheaper the rent, the higher the return.

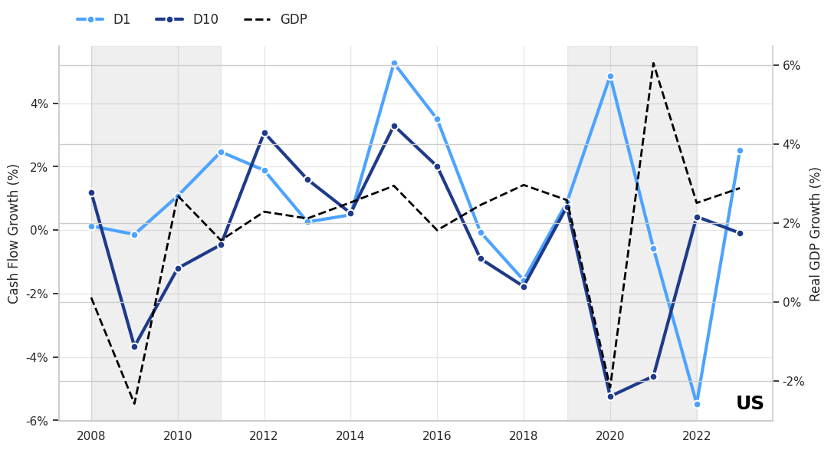

Systematic Risk? More Hedge Than Hazard

A natural suspicion is that these higher returns compensate for higher risk. The data suggest the opposite: In downturns, affordable rentals act as a hedge. Cash flows from low-rent units actually rise during recessions as households trade down. Instead of being riskier, low-rent housing looks more stable.

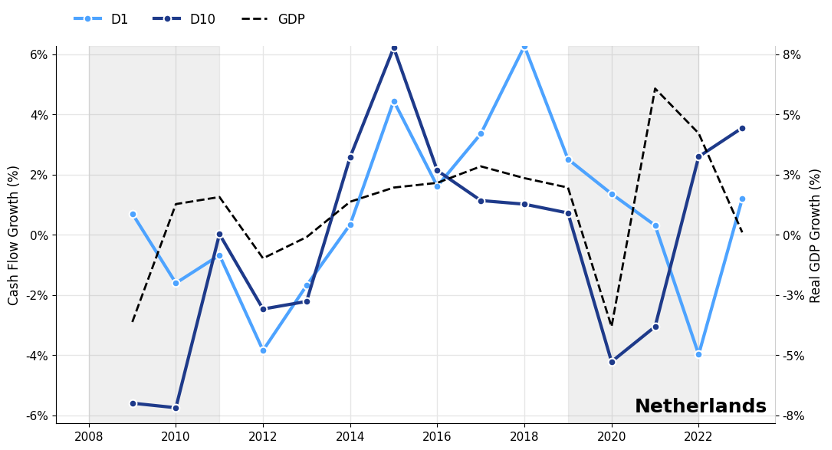

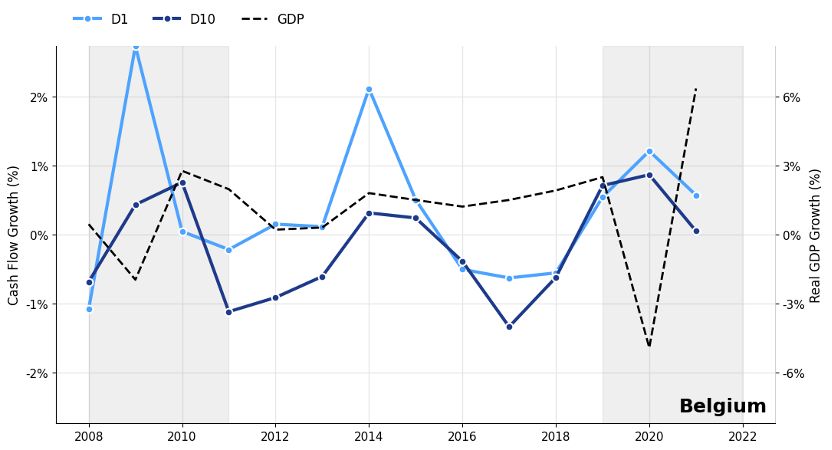

- Recession Hedge: During the 2008 financial crisis and the COVID-19 recession, cash flows at low-rent multifamily properties actually increased while higher-rent units saw declines. Affordable rentals function as a recession hedge. The figures below illustrate this pattern: in the US, median net cash flow growth at low-rent properties held up or even rose as GDP contracted, with similar resilience visible in the Netherlands and Belgium.

- The Trade-Down Effect: Shelter comes with a floor—households can cut back on dining or travel, but they can’t cut back on housing. When incomes tighten, they don’t exit the rental market; they simply trade down. That “downgrade demand” flows straight into affordable units, giving them a natural cushion.

Regulatory Risk? Not the Driver

Another natural suspicion is that stronger tenant protections and rent control measures increase downside exposure in the low-rent segment. If regulatory risk were really driving the return premium, one would expect steeper return–rent slopes and higher compensation in jurisdictions with more regulation. However, the data show otherwise.

- Policy Slope: Across US states, stronger renter protection laws are associated with flatter, not steeper, return–rent slopes.

- No Premium in High-Regulation States: States with greater legal protections for tenants do not offer higher total returns in low-rent segments. The same is true when we compare states where local rent control is possible versus where it is illegal.

- International Context: In the Netherlands, tighter rent ceilings do not correspond to stronger return gaps.

Idiosyncratic Risks? No Evidence

A further possibility is that low-rent units are simply riskier on a property-by-property basis. The evidence again points in the opposite direction.

- Mortgage Performance: Delinquency rates are not higher at the bottom. In fact, the lowest-rent multifamily loans show similar performance to mid- and high-rent segments.

- Cash-Flow Volatility: Over realistic holding periods of 3-5 years, cash-flow growth is hardly more volatile at the bottom than at the top.

- Landlord Diversification: Low-tier properties in both Belgium and the Netherlands are typically held by medium-sized owners who own dozens of assets, limiting idiosyncratic risk exposure.

Why Don’t Investors Pile In?

If excess returns exist, why hasn’t capital flown into this market? The answer lies in frictions that prevent arbitrage:

- Tenants Can’t Buy: Low-income renters are financially constrained. Down payments, mortgage access, and unstable earnings make ownership challenging. Many low-rent units are in large apartment blocks, further limiting individual purchase opportunities.

- Large Institutions Stay Away: Big corporate landlords avoid the low-rent market. Part of this is out of concern for their reputation—no pension fund wants to be accused of “slumlord” practices. Another part is management diseconomies: low-income tenants and older properties require intensive oversight, which are difficult to scale efficiently.

- Medium-Sized Landlords Can’t Scale: Local, mid-sized landlords dominate this segment. While they do earn higher returns, they face capital constraints. With little access to equity markets, they rely on retained earnings to finance expansion. Moreover, they display a strong local bias, investing close to home rather than reallocating capital across regions.

The result is an equilibrium in which excess returns persist—not because the opportunity is invisible, but because only a narrow set of investors can access it.

Policy Implications: Unlocking the Alpha

If low-rent housing provides both social benefits and financial alpha, policy should aim to reduce the frictions that block capital flows:

- Mobilize Institutional Capital: US programs like Opportunity Zones, Freddie Mac’s Workforce Housing initiatives, and Florida’s Live Local Act have encouraged large-scale investment in affordable rentals. Similar targeted incentives could work in Europe, where institutional capital is scarcer in the low-rent segment.

- Support Medium-Sized Investors: Public-private partnerships could design equity co-investment funds that partner with local landlords, helping them expand portfolios without excessive leverage. Nationally diversified housing funds could offset local bias.

- Empower Tenants: Shared equity programs, first-time buyer credits, or tenant purchase rights could enable renters to transition into ownership. These policies would redirect some of the high returns back to the households currently paying them.

- Expand Supply: While new construction of affordable units is costly, expanding supply in higher-rent segments can ease pressures through filtering.

Conclusion: A Hidden Alpha, A Social Cost

The evidence is unambiguous: low-rent housing delivers high risk-adjusted returns. Yet frictions in financing, institutional participation, and tenant purchasing power prevent these gains from being arbitraged away.

Affordable housing thus sits at the intersection of social policy and financial opportunity. For policymakers, the task is to harness this hidden alpha—channeling more capital into the sector, lowering costs for tenants, and ensuring that housing, the most basic of necessities, does not remain the most expensive for those least able to pay.

FAQs:

Q: Why do low-rent properties deliver higher returns?

A: Because demand for affordable housing stays strong in all economic cycles. Lower-rent units earn higher yields and appreciate faster than high-end properties.

Q: Are these higher returns the result of higher risk?

A: No. Data show that low-rent properties are more stable during recessions, as tenants “trade down” rather than leave the market entirely.

Q: Why haven’t investors flooded into affordable housing?

A: Frictions block capital flow. Institutional investors avoid the reputational and management challenges, while smaller landlords lack access to growth capital.

About the Contributor:

Stijn Van Nieuwerburgh is the Earle W. Kazis and Benjamin Schore Professor of Real Estate and Professor of Finance at Columbia University’s Graduate School of Business, which he joined in July 2018 after 15 years at New York University’s Stern School of Business. He earned his PhD in Economics (2003), MSc in Financial Mathematics (2001), and MA in Economics (2001) from Stanford University, and a B.A. in Economics from the University of Ghent, Belgium (1998).

His research lies in the intersection of real estate, asset pricing, and macroeconomics. He studies the impact of remote work on real estate valuations, affordable housing policies, mortgage market design, the impact of foreign buyers on the housing market, property price dynamics, and mortgage choice. Another recent strand of his research focuses on government debt and fiscal policy. His has published over 50 articles in peer-reviewed journals and his work is frequently covered in the media, including on 60 Minutes, the New York Times, the Wall Street Journal, the Economist, and the Financial Times. Full bio here.